Quick education for old 401(k), IRA rollover, direct rollover, tax-rule awareness, income planning, and account organization before you make retirement decisions.

A rollover decision can affect taxes, account access, investment choices, fees, beneficiaries, and retirement income planning. Start with education before choosing a path.

Rollovers may involve employer plans, IRAs, pre-tax assets, Roth assets, after-tax dollars, or plan-to-plan transfers. The rules depend on the account type and plan provider.

A former workplace plan may offer several choices. Some families leave assets in the old plan, move them to a new employer plan, roll to an IRA, or consider a distribution after understanding tax consequences.

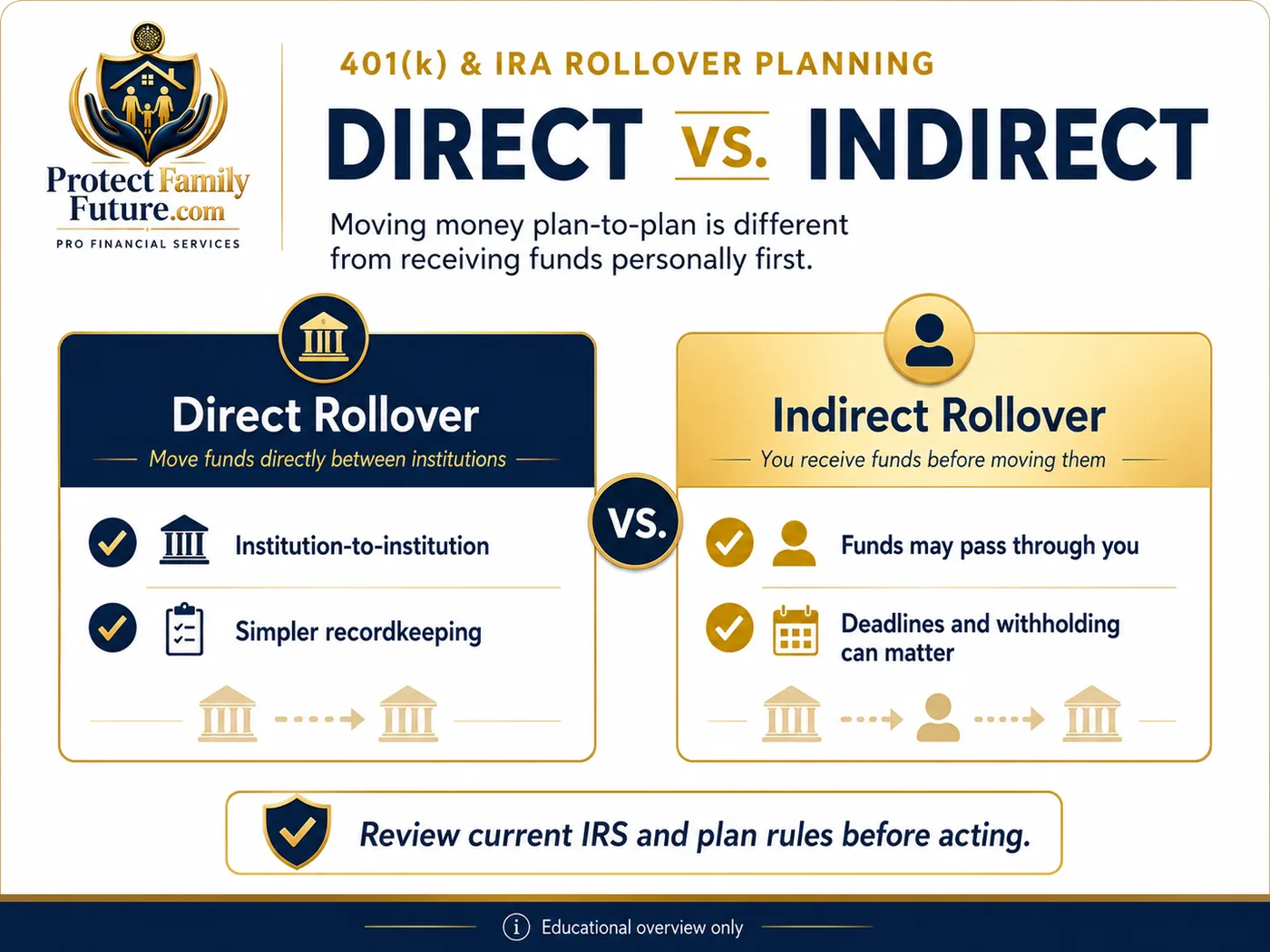

A direct rollover generally means the funds move from the current plan to the receiving plan or IRA without being paid to you personally. This can help avoid withholding issues tied to indirect rollovers.

Indirect rollovers can create additional steps. Employer-plan distributions paid to you may be subject to mandatory withholding, and the full rollover generally must be completed within the allowed timeframe.

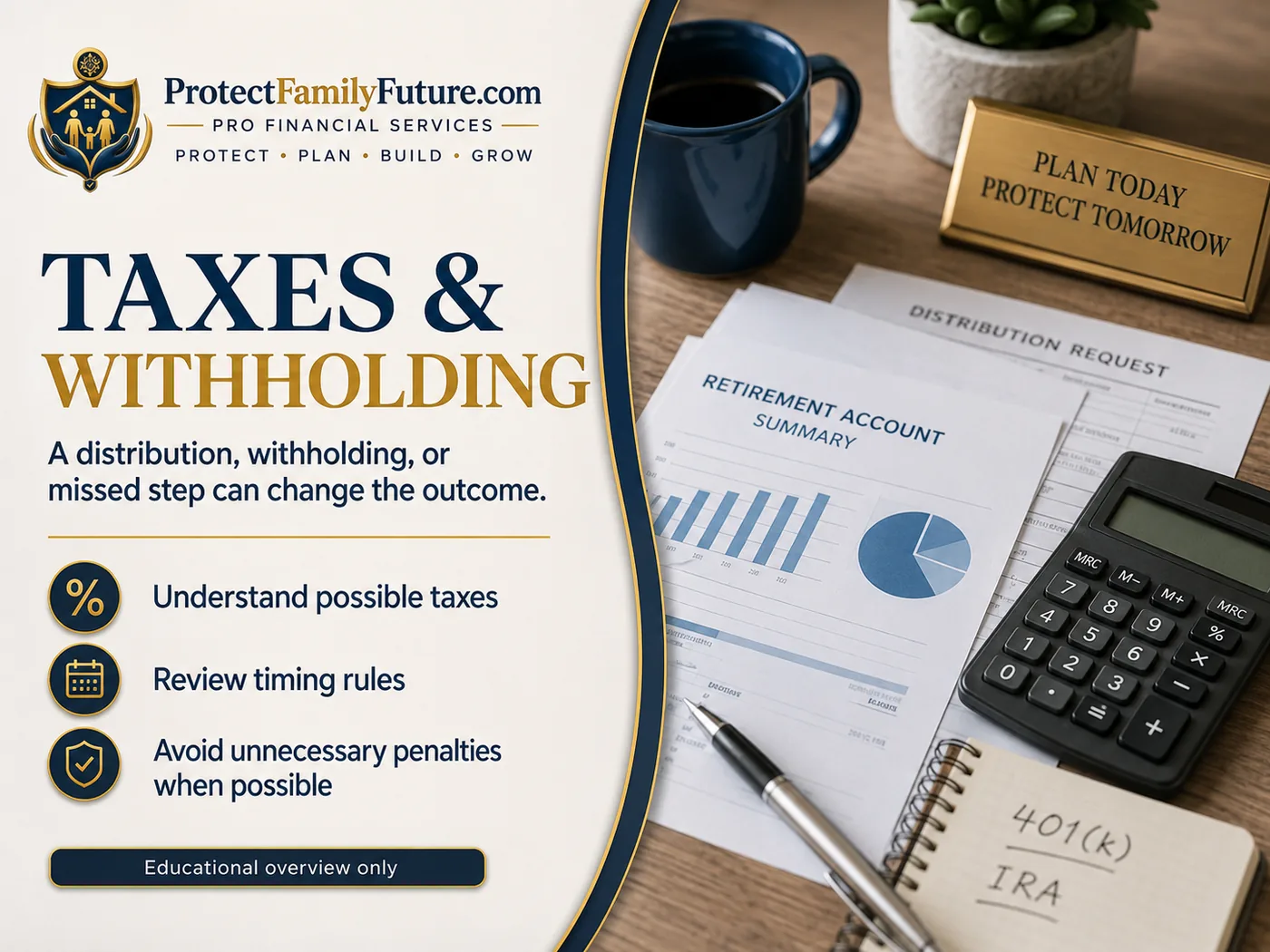

Before moving retirement money, identify whether the assets are pre-tax, Roth, after-tax, employer match, or mixed-source dollars. Rolling or converting to a different tax category may have tax consequences.

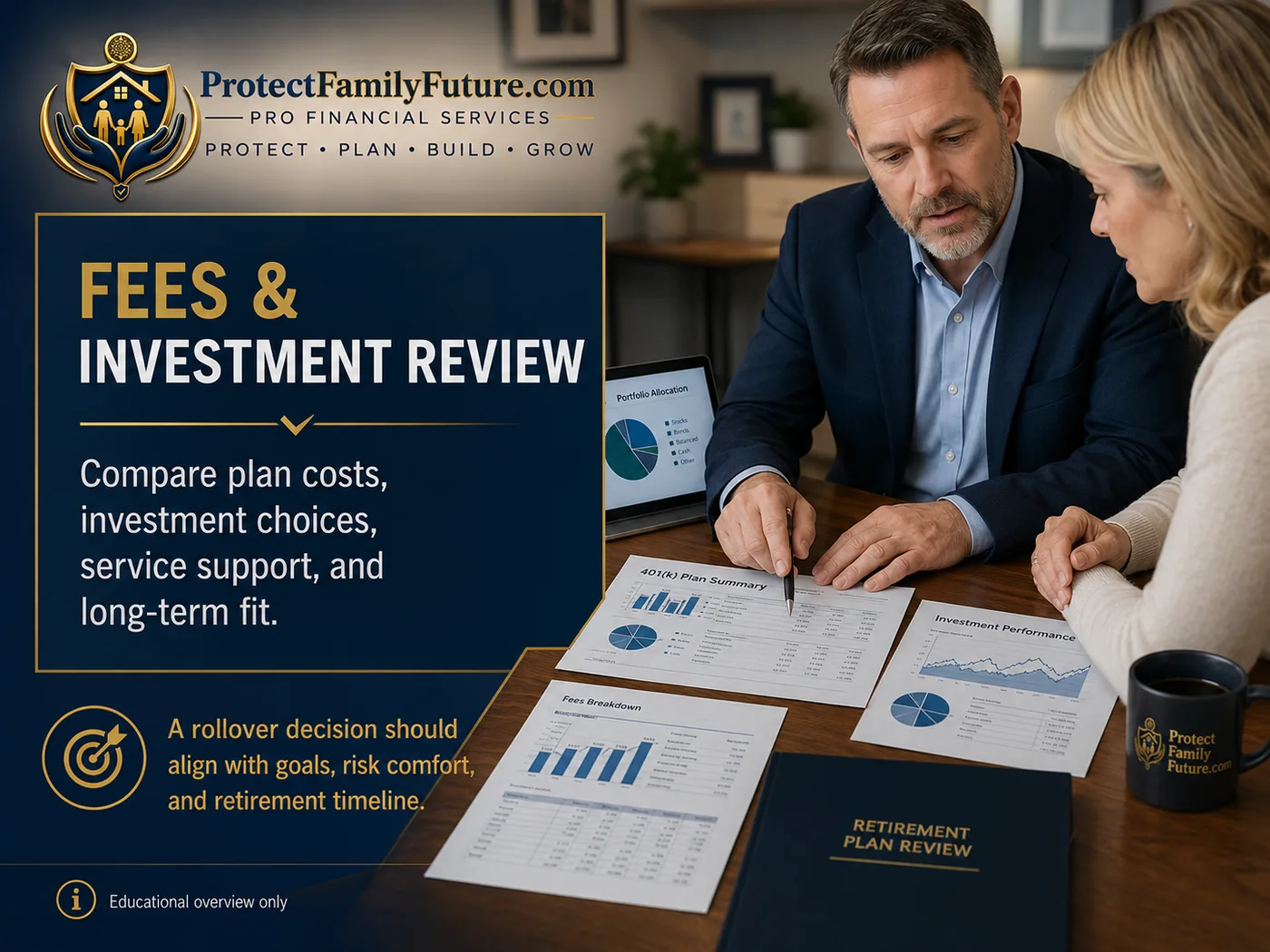

Retirement decisions should compare investments, plan costs, advisory costs, services, creditor protections, withdrawal rules, and account features—not just convenience.

Retirement planning is moving from account accumulation toward sustainable income planning. A rollover review should fit the bigger picture of future monthly income and cash-flow needs.

Changed jobs, family changes, old beneficiaries, and multiple statements can make retirement accounts harder to manage. A review can organize accounts before important choices are needed.

Start with a simple conversation. We help you organize accounts, understand rollover questions, and prepare a checklist before you make retirement-account decisions.

Share your details and we will help you choose the right education starting point for your old 401(k), IRA, or retirement income questions.

Review the key items that may affect taxes, savings, account organization, investment fit, income timing, and family clarity before moving retirement money.

Before moving retirement money, understand whether the transaction is a direct rollover, indirect rollover, Roth conversion, taxable distribution, or another type of transfer.

A direct rollover typically sends funds to the receiving institution, while an indirect rollover may pay you first and create additional timing and withholding responsibilities.

Employer plans may have specific rules for investments, loans, withdrawals, creditor protection, employer stock, plan fees, and when former employees can move money.

Compare the total cost and available investment menu before deciding. A rollover may simplify management, but costs and choices can change.

The tax character of each dollar matters. Pre-tax, Roth, and after-tax balances may require different rollover paths and records.

Required minimum distributions, age 55 workplace-plan rules, early-distribution rules, and still-working exceptions can all affect the right planning questions.

A strong rollover review connects account choices with future monthly income, withdrawal needs, Social Security timing awareness, healthcare costs, and household cash flow.

Consolidation can reduce statements and confusion, but families should also review fees, beneficiary designations, tax character, plan features, and creditor protections.

A rollover decision should fit how soon income is needed, how much risk the family can tolerate, and how the account supports long-term goals.

Before moving retirement money, prepare a checklist for your plan provider, IRA custodian, tax professional, legal professional, and financial professional where needed.

Send your details and we will help you organize the questions to review before moving or consolidating retirement accounts.

If you changed jobs, retired, or have multiple workplace retirement accounts, your next step should be based on education, plan rules, tax awareness, fees, investment choices, timing, and long-term retirement-income goals.

Common choices may include keeping the account in the old employer plan if allowed, moving it to a new employer plan if accepted, rolling it to an IRA, or taking a cash distribution. Each path should be reviewed carefully before action is taken.

Changed jobs, preparing for retirement, or managing multiple workplace accounts can create decisions about fees, tax rules, investment options, account access, beneficiaries, and future income.

May maintain current plan features, if allowed.

May consolidate into a new workplace plan, if accepted.

May provide account consolidation and broader investment choice.

May trigger taxes and penalties. Usually requires careful review.

Changing jobs, retiring, or holding multiple old workplace accounts can feel simple at first, but rollover choices may affect taxes, investment options, withdrawal rules, RMDs, creditor protections, and family coordination. Start with education, then decide with qualified guidance.

Old 401(k), IRA, Roth, pension, annuity, Social Security, and other resources.

Stay in plan, move to new plan, roll to IRA, or take a distribution.

Fees, investment choices, withdrawal rules, RMDs, loans, taxes, and protections.

Estimate retirement cash flow, emergency needs, health costs, taxes, and legacy goals.

Review the core topics before choosing a rollover path or changing retirement accounts.

A rollover generally moves retirement assets from an employer-sponsored plan, such as a 401(k), 403(b), or 457(b), to another eligible plan or IRA. Direct rollovers are commonly used to avoid unnecessary withholding and deadline issues.

Learn MoreCommon choices include leaving assets in the former plan if allowed, moving to a new employer plan if accepted, rolling to an IRA, or taking a distribution. Each choice can have different tax, fee, investment, and withdrawal implications.

Indirect rollovers can involve the 60-day deadline and withholding. Traditional, Roth, and after-tax amounts can have different treatment. Tax questions should be reviewed with qualified tax professionals.

Retirement planning should connect account balances to monthly income, Social Security timing, withdrawals, RMD awareness, healthcare needs, emergency reserves, and family goals.

Gather plan statements, account type details, beneficiary information, fees, investment lineup, loan information, and current provider transfer instructions before deciding.

Rollover and retirement-income decisions can involve taxes, penalties, plan rules, time limits, investment selection, fees, and beneficiary coordination. Education helps families slow down and ask better questions.

Old accounts may become harder to track and coordinate with retirement goals.

Indirect rollovers may trigger the 60-day rule and withholding issues.

Pre-tax, Roth, and after-tax money should be reviewed before transfer.

Account balances should connect to retirement cash-flow needs.

There is no one-size-fits-all rollover choice. Plan features, fees, investment options, loans, withdrawal rules, tax treatment, RMDs, and creditor protections can vary.

| Feature / option | Keep old plan | Move to new plan | Rollover IRA | Cash distribution |

|---|---|---|---|---|

| Investment choices | Plan menu | New plan menu | IRA platform options | N/A after withdrawal |

| Fees | Vary by plan | Vary by plan | Vary by provider/investments | Taxes/penalties may apply |

| Loan options | May be limited/not available after leaving | May be available if plan allows | Not available in IRA | N/A |

| RMDs | Rules may vary | Rules may vary | Generally apply to traditional IRAs | Distribution tax rules apply |

| Ease of management | Multiple accounts | Potential consolidation | Potential consolidation | Retirement funds removed |

A direct rollover is generally paid directly from the old retirement plan to the new eligible plan or IRA. An indirect rollover is paid to you first and may involve withholding and a 60-day redeposit rule.

Retirement planning is not only about balances. It is about income sources, timing, taxes, healthcare, emergency needs, and family goals.

Account-based retirement savings and rollover decisions.

Timing awareness and household income coordination.

Review any employer pensions, annuities, or business income.

Emergency savings and short-term stability for withdrawals.

Use this placeholder for your YouTube education video.

Book After WatchingLet’s review your goals, accounts, and options so you can make the right decision with more confidence.

Book Discovery CallWhatsApp / Text UsCall (732) 318-8662100% Private • No Pressure • Educational

A rollover generally moves retirement assets from an employer plan to another eligible retirement plan or IRA.

If an eligible distribution is paid to you, you generally have 60 days to roll it over. Direct rollovers are commonly used to avoid this issue.

It depends on plan features, fees, investment choices, withdrawal rules, creditor protection, tax treatment, and your personal goals.

Traditional/pre-tax and Roth/after-tax assets can have different tax treatment and destination account rules.

Gather your latest statement, account type, beneficiary info, and call us for an education review.

If you cannot call now, fill out this form. We will contact you to help with retirement and rollover education questions.

Education today helps you protect tomorrow. We are here to guide you with clarity, care, and experience.

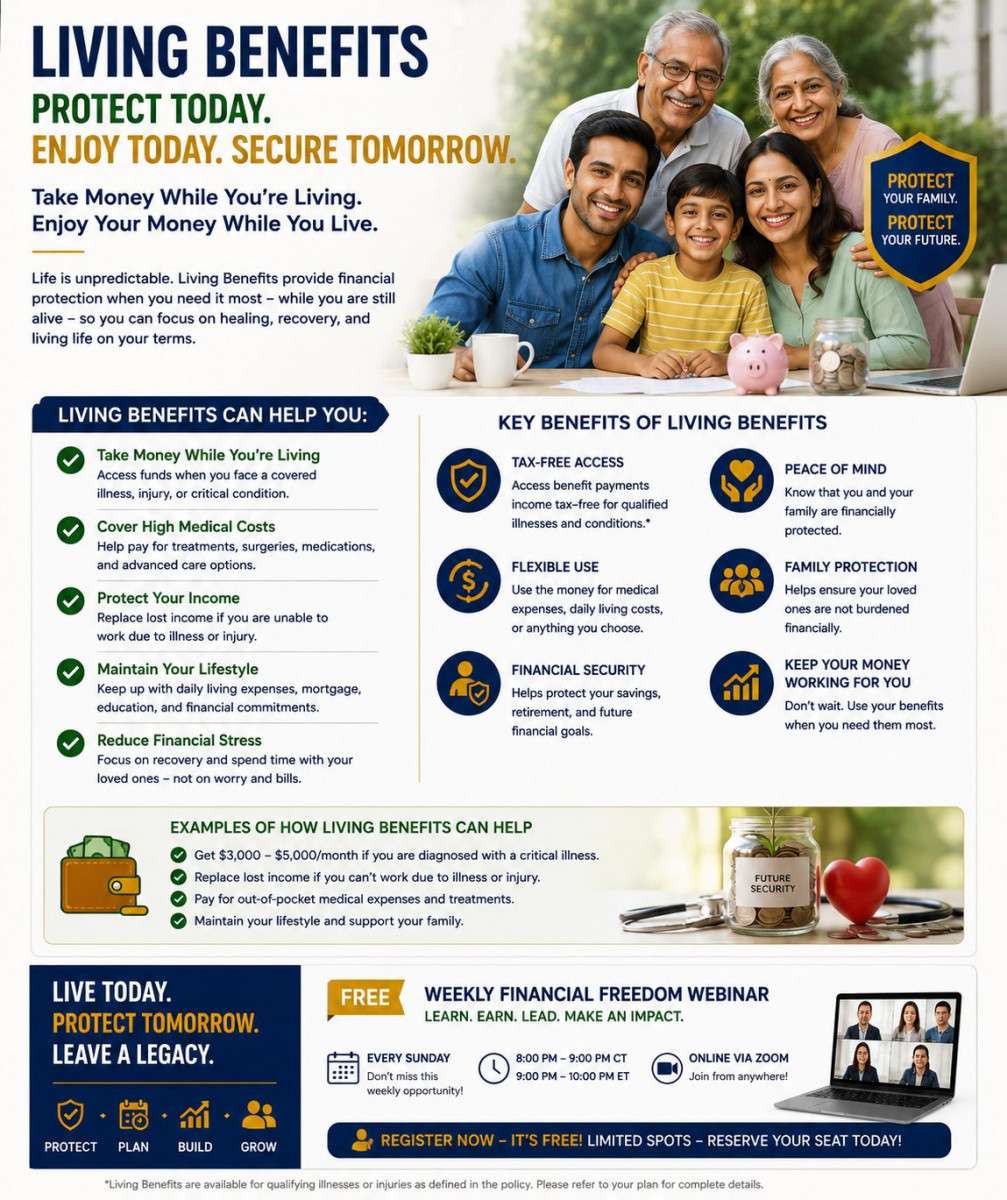

Living Benefits Planning is not only about life insurance after death. It helps families understand whether a policy may include features that can provide access to benefits during qualifying health events, and how those features may affect income, bills, caregiving, and the protection left for loved ones.

Families often assume life insurance only matters after death, or assume living benefits automatically apply. A serious illness, chronic care need, terminal diagnosis, or income disruption can create urgent questions before the family has reviewed the policy.

A serious health event may reduce income while housing costs, utilities, debt, groceries, and family obligations continue.

Living benefits education helps families ask how policy features may fit with income replacement, emergency savings, and dependent care planning.

When a loved one becomes seriously ill, caregiving responsibilities may affect work schedules, household routines, and family finances.

Self-employed professionals and business owners may need to review how a serious illness could affect revenue, operations, and family cash flow.

Policy wording may treat critical illness, chronic illness, terminal illness, and long-term care-related provisions differently.

Using accelerated benefits during life may reduce the death benefit or other policy values available later, so families should understand the tradeoff.

Start with a simple education call and a policy review checklist. We will help you identify what to organize, which living benefits questions to ask, and where qualified professionals may be needed.

Schedule a private educational discovery call to review living benefits concepts, policy questions, rider awareness, health-event planning, and family protection priorities before a crisis happens.

This call helps you understand what to organize, which questions to ask, and how living benefits may fit into a broader family protection plan. We keep the conversation educational, private, and simple.

Select an available date and time for your Living Benefits Planning education call. Your confirmation and meeting details will be sent automatically.

If the calendar does not load inside this page, open the booking calendar directly.

Open Booking CalendarSend your contact details. If your preferred calendar time is not available, we will help you find the right next step for your Living Benefits Planning review.

Protect • Plan • Build • Grow

Explore education-first family protection planning designed to help families prepare for income protection, mortgage protection, final expenses, and long-term family security.

Learn how will and trust planning, estate planning, beneficiary preparation, and family asset protection conversations can help loved ones move forward with clarity.

Explore child future planning concepts designed to help families understand long-term growth potential, early planning, family protection, and legacy-building strategies.

Explore college savings planning, 529 plan education, education savings strategies, student loan burden awareness, and child future planning for families.

Living benefits education helps families understand how some protection strategies may provide access to benefits while still living during qualifying health events.

Explore tax-efficient growth, tax-advantaged income, retirement income planning, and legacy planning strategies designed to help families make smarter long-term decisions.

Start with a simple educational conversation. We’ll help you understand your goals and guide you toward the right financial education topic or next step.

Share your details and we’ll help you choose the right starting point.

Help protect your loved ones from life’s unexpected events with customized solutions.

Learn More

Create reliable income for retirement and enjoy the lifestyle you’ve worked for.

Learn More

Access benefits while you’re living and protect your wealth and health.

Learn More

Build a brighter future for your children with smart education and financial planning.

Learn MoreTop recommended education areas for complete family 360° protection.

Explore essential education areas for family protection, children’s future planning, living benefits, health challenges, retirement strategies, and will & trust legacy planning..

Discover how family protection planning can help create confidence today and tomorrow.

LEARN MORE

Learn how early planning may help build a stronger foundation for a child’s future.

LEARN MORE

Explore education funding ideas designed to support children’s dreams and opportunities.

LEARN MORE

Help protect your wishes, loved ones, and legacy for future generations.

LEARN MORE

Learn how living benefits may help provide support while you are living, not only after death.

LEARN MORE

Explore planning options that may help during qualifying health events.

LEARN MORE

Explore tax-aware retirement strategies designed to help protect long-term income.

LEARN MORE

Review rollover, retirement income, and protection strategies for long-term security.

LEARN MOREExplore our education-first pathways for family protection, business opportunity, leadership development & community impact.

Protect what matters most.

Explore strategies designed to help safeguard your family’s future and create long-term confidence.

Learn More →

Earn. Lead. Impact. Freedom.

Create additional income and build a purpose-driven path while helping families.

Explore Opportunity →

Develop. Grow. Succeed.

Build leadership skills, unlock your potential, and create lasting impact.

Join Leadership Academy →

Serve. Educate. Empower.

Build stronger communities today while helping families prepare for a better tomorrow.

Make an Impact →

Learn how certain life insurance policy features may help during qualifying illness, how riders may be reviewed, and what families should understand before assuming a policy can be used while living.

If you cannot call now, use the form below or send a WhatsApp message. We will help you choose the right education path.

Book Discovery Call WhatsApp / Text Now Call / Text: (732) 318-8662Living benefits are policy features or riders that may allow access to a portion of benefits while the insured is living, usually only after certain qualifying health events and claim requirements are met.

No. Availability depends on the policy type, rider language, carrier, state, underwriting, and when the policy was issued. Older policies may not include the same features as newer policies.

Some policies may address terminal illness, chronic illness, critical illness, or long-term care-related situations. The exact definitions, limits, and claim requirements vary by policy and rider.

No. Living benefits are not health insurance and should not be treated as a replacement for medical coverage, disability coverage, long-term care coverage, or emergency savings.

Yes, accessing benefits during life may reduce the remaining death benefit, cash value, loan value, or other policy values. Families should review the impact before making decisions.

If available, gather your policy summary, rider pages, beneficiary page, premium information, recent statement, and carrier contact details.

Fill out the form, send a WhatsApp message, or text/call (732) 318-8662. We will follow up and help you choose the right next step.

If you cannot call now, fill out this form. We will contact you to help with your Living Benefits education questions.

Let’s review your goals, current policy questions, and how your family may prepare before a serious health event creates pressure.

Book Discovery Call WhatsApp / Text Now Call (732) 318-8662